Restaurant payment solutions are systems that integrate secure payment processing directly into a restaurant’s point of sale and management platforms, unifying transaction data, order records, and financial reporting in one place. For UK operators running anything from a busy city-centre café to a multi-site restaurant group, choosing the wrong setup creates daily friction: manual reconciliation errors, mismatched end-of-day reports, and customers waiting too long to pay. The difference between a basic card terminal and a fully embedded payment system is not cosmetic. It determines how accurately your business tracks revenue, handles refunds, and manages cash flow. This guide covers payment processing for restaurants from the ground up, so you can make an informed decision.

What are the main types of restaurant payment solutions?

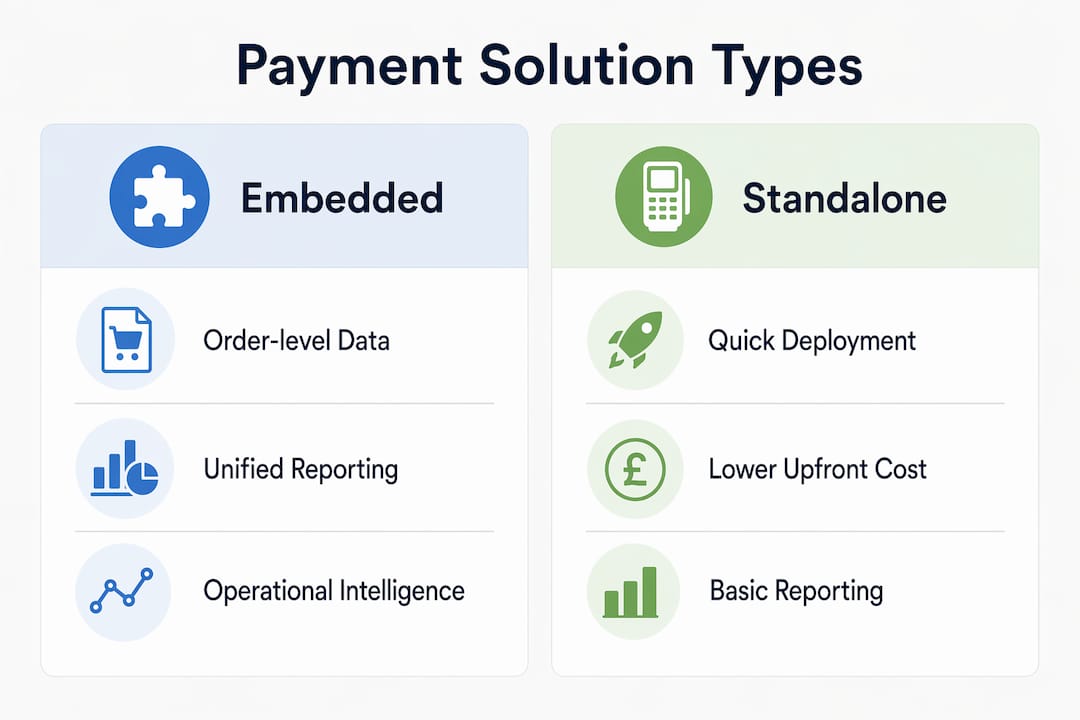

Payment processing for restaurants falls into three broad categories, each with distinct operational implications.

Embedded payments run processing through the restaurant’s own POS or management platform. Settlement and reports flow back to the same system handling orders and modifications, which eliminates the gap between what was ordered and what was charged. Stripe Terminal is the most widely cited example of this architecture in the UK market.

Standalone terminals accept card payments independently of any POS system. They are quick to deploy and inexpensive upfront, but they produce a separate transaction record that must be manually matched to your order management data. For high-volume services, this creates a reconciliation burden every single day.

Platform payments sit between the two. They are common in delivery marketplaces and multi-operator venues where payment processing design affects risk profiles across aggregated flows. They offer flexibility but introduce complexity around settlement timing and liability.

The table below summarises the key differences:

| Solution type | Integration depth | Reconciliation | Best suited for |

|---|---|---|---|

| Embedded payments | Full order-level | Automated | Full-service and fast-casual restaurants |

| Standalone terminal | None | Manual | Low-volume or pop-up operations |

| Platform payments | Partial | Semi-automated | Delivery platforms, multi-operator venues |

| Mobile/QR code payments | Varies by provider | Depends on POS link | Table-service and self-order environments |

Key capabilities to look for across all types include:

- Contactless acceptance for chip, tap, and mobile wallet payments

- Split payment handling by item, percentage, or equal share

- Tip and gratuity configuration at the point of payment

- Real-time reporting accessible from the same dashboard as your orders

The right choice depends on your service model, but for most full-service restaurants, embedded or deeply integrated solutions deliver the strongest operational return.

How does integration depth affect reconciliation and reporting?

Integration depth is the single most consequential technical decision in restaurant payment processing, yet it is routinely underestimated during procurement.

A shallow integration records only the total charged. It does not capture which items were on the bill, whether a discount was applied, or how a split was divided. Integration failures most commonly occur at the accounting and reconciliation level rather than at checkout. The terminal processes the payment without error, but the back-office data is incomplete, forcing staff to cross-reference paper receipts or POS logs manually.

Order-level integration changes this entirely. When a payment is linked to specific line items, modifiers, and discounts, every chargeback, refund, or void carries the full context of the original transaction. Your accounts team can resolve disputes in minutes rather than hours. End-of-day reporting becomes a check rather than a reconstruction.

“The primary value of embedded payments extends beyond faster checkout to seamless integration of payment data with orders, enabling more accurate financial tracking and decisions.” — Stripe

Pro Tip: Before signing any payment processing contract, ask the provider to demonstrate how a split-bill refund appears in your reporting dashboard. If the answer involves a separate reconciliation step, the integration is shallower than you need.

Unified data from embedded payments also surfaces operational intelligence that standalone terminals cannot provide. Sales patterns such as top-performing menu items, table turns, and revenue distribution by time of day become visible when payment data is tied to order management. That information directly informs staffing, menu pricing, and promotional decisions.

Which features should you prioritise when choosing a payment solution?

Selecting the best restaurant payment systems requires evaluating features against your specific service model, not a generic checklist. The following priorities are ranked by operational impact.

-

Payment method coverage. Contactless and mobile wallet payments including Apple Pay and Google Pay are now baseline expectations for UK diners. Any solution that requires separate hardware negotiation to accept these methods adds unnecessary complexity and cost.

-

Split payment logic. Restaurant-native payment stacks must handle splits and tips within the system logic to minimise errors and manual interventions. Look for solutions that support splits by item, by equal share, and by custom percentage without requiring staff to perform manual calculations.

-

Tip and gratuity configuration. The ability to present tip prompts at configurable percentages directly on the payment terminal affects both customer behaviour and staff earnings. This feature must be built into the payment flow, not added as an afterthought.

-

Hardware compatibility. Your payment terminals must work reliably with your existing POS hardware. Incompatible devices create service delays and support headaches. Ycr distributes hardware from SAM4S and iMin that is designed for exactly this kind of integrated hospitality environment. Reviewing POS hardware types before committing to a payment provider prevents costly mismatches.

-

Settlement timing. Settlement times and payout schedules vary by provider and directly affect your ability to meet payroll and pay suppliers on time. A provider offering next-day settlement gives you materially better cash flow control than one operating on a three-day cycle.

-

Support and vendor reliability. Payment outages during a Friday dinner service are not a minor inconvenience. They are a direct revenue loss. Assess the provider’s uptime record, support response times, and whether UK-based telephone support is available during trading hours.

How do popular restaurant payment systems compare?

The restaurant payment options comparison below focuses on the systems most relevant to UK operators in 2026, evaluated on customer experience impact and operational efficiency.

| System / feature | Table turn speed | Wallet support | Order-level data | Split payments |

|---|---|---|---|---|

| Stripe Terminal (embedded) | High | Yes (Apple Pay, Google Pay) | Full | Yes |

| Standalone card terminal | Standard | Limited | None | Manual |

| QR code / pay-at-table | Very high | Yes | Depends on POS link | Yes |

| Platform payment (marketplace) | Variable | Yes | Partial | Limited |

Shortening table turnover by five minutes compounds to meaningful business impact across a full service. A 60-seat restaurant turning tables five minutes faster during a two-hour dinner service can accommodate an additional seating across the week without adding a single cover.

QR code payments deserve particular attention. When linked to an integrated POS, they allow guests to order, reorder, and pay without waiting for staff. The guest experience improves, and the data captured is as rich as any table-side terminal transaction. The critical caveat is that QR code systems only deliver this value when the underlying POS integration is order-level, not total-only.

Switching costs are a genuine risk when evaluating top payment platforms for dining. The deeper the integration, the harder it is to replace components without disrupting data history and operational continuity. This is not a reason to avoid deep integration. It is a reason to choose your provider carefully from the outset, using a structured process like the one outlined in Ycr’s guide to choosing a POS system for UK restaurants and retail.

Integrating payment solutions with your existing POS also affects how you handle digital payment methods going forward. As contactless and wallet payments continue to displace cash in the UK, operators without a unified payment and order platform will find reporting increasingly fragmented.

Key takeaways

Choosing the right restaurant payment solution requires order-level integration, hardware compatibility, and a clear understanding of settlement timing to protect both service quality and cash flow.

| Point | Details |

|---|---|

| Embedded payments outperform standalone terminals | Order-level data enables automated reconciliation and eliminates manual end-of-day matching. |

| Integration depth determines reporting accuracy | Shallow integrations record totals only, creating reconciliation gaps that cost time and money. |

| Split payments and tips need native system support | Manual calculations at the terminal increase errors and slow table service. |

| Settlement timing affects cash flow directly | Choose a provider with next-day settlement to maintain reliable payroll and supplier payments. |

| Switching costs rise with integration depth | Select your payment provider carefully upfront, as deep integrations are difficult to replace without disruption. |

Why I think most operators underestimate the back-office problem

After years of working with hospitality operators across the UK, the pattern I see most often is this: a restaurant invests in a capable POS system, then connects it to a payment terminal that records only the total charged. The checkout works perfectly. The reconciliation is a nightmare.

The instinct to separate payment hardware from POS software to save money is understandable. But the cost of that decision shows up every evening when someone has to manually cross-reference terminal reports against order data. Multiply that by 300 trading days and you have a significant labour cost that never appears on the original procurement spreadsheet.

What I find genuinely underappreciated is how much operational intelligence disappears with a shallow integration. Knowing that your 7pm sittings generate 40% more revenue per cover than your 6pm sittings is the kind of insight that changes pricing and staffing decisions. That data exists in your orders. It only becomes visible when your payment system is reading from the same source.

The vendor lock-in concern is real but manageable. The answer is not to avoid deep integration. The answer is to do the selection work properly at the start, verify that your hardware and software are genuinely compatible, and build a relationship with a distributor who understands both sides of the stack.

The operators I have seen get this right share one habit: they test reconciliation before they go live, not after.

— John

Explore POS hardware and software built for restaurant payments

Ycr supplies the hardware and software that make integrated restaurant payment processing work in practice. From SAM4S and iMin POS terminals to SAMTOUCH and EZEEPOS software, every product in the Ycr catalogue is selected for compatibility with embedded payment environments. If you are building or upgrading a payment stack, understanding the hardware layer is the logical starting point. Ycr’s POS hardware terminology guide covers the components that directly affect payment speed and reliability, and the POS software range details the software solutions designed specifically for UK hospitality operators. Next-day delivery and same-day dispatch mean your operation does not have to wait.

FAQ

What is the difference between embedded and standalone payment solutions?

Embedded payments process transactions through your POS or management platform, linking payment data directly to order records for automated reconciliation. Standalone terminals process payments independently, producing a separate record that must be manually matched to your order data.

How does order-level integration improve restaurant reconciliation?

Order-level integration attaches each payment to specific line items, discounts, and modifiers, so refunds, voids, and chargebacks carry full transaction context. This removes the need for manual cross-referencing and significantly reduces end-of-day accounting errors.

Which payment methods should a restaurant solution support?

A modern restaurant payment solution must accept chip and PIN, contactless, and mobile wallets including Apple Pay and Google Pay. Solutions that require separate hardware to support wallet payments add unnecessary cost and complexity.

How do I choose between payment solutions for my restaurant?

Evaluate solutions on integration depth, split payment handling, tip configuration, hardware compatibility, and settlement timing. Ycr’s restaurant payment processing guide provides a structured framework for UK operators making this decision.

Do QR code payments work as well as terminal payments for restaurants?

QR code payments deliver equivalent data quality to terminal payments only when they are linked to an order-level POS integration. Without that link, they record totals only and create the same reconciliation gaps as standalone terminals.